Franking credits – The quiet engine of Australian retirement income

SOURCE: Empire Financial Group

BY: Raymond Pecotic

October 6, 2025

(This article was first published in The West Australian, YourMoney, on 6 October 2025)

Retirement is meant to be the reward for decades of work and saving. But anyone drawing an income from their super knows the reality – these days every dollar needs to be stretched further. Rising living costs and longer lifespans make reliable cash flow essential. Despite the Reserve bank holding firm on interest rates this month, rates are still likely to trend down over the next year or so, so the hunt for yield is only intensifying.

Higher returns often mean higher risk. But there is a way to get a boost on yield by making subtle changes to your portfolio that don’t necessarily mean more risk.

That’s where franking credits step in.

Why yield matters in retirement

Those still in the workforce and contributing to their retirement pot can ride out volatility and reinvest for growth. However, retirees need regular, spendable income. But a portfolio also needs growth to keep ahead of inflation. That’s where a blend of growth assets like shares and property is mixed with yield assets such as bonds and even term deposits. Not too long ago, term deposits offered rates well into the 5% per cent, and even 6% on cash in the bank. Today, they hover around 4%, and government treasuries less than that, with an expectation that could trend lower in the short to medium term.

If you can’t get yield from cash and bonds, you look elsewhere. For many retirees, that means dividend paying shares.

But are all shares created equal? And if looking for yield, should you buy Australian or international shares.

There are much wider considerations when making that decision, but one factor in favour of Australian shares is the humble franking credit.

The franking credit effect

When Australian companies pay dividends, they attach franking credits – recognition of the tax already paid on profits, which is usually at 30%. When the dividend income is paid to you, and your tax return is done at the end of the year, you either need to top up tax or get a refund, depending if your tax rate is higher or lower than 30%. For retirees who hold assets in the superannuation pension phase, where the tax rate is 0%, those credits aren’t just offsets. They’re refunded in cash.

Take a company that earns $1,000 profit. It pays $300 tax to the ATO, then pays you (via your super pension account) a $700 dividend. Alongside it comes a $300 franking credit. Because your tax rate is 0% and you owe no tax, the ATO refunds the $300. The end result in your pocket is the full $1,000. That’s a 43% boost to your income, simply from the way the system is designed.

Comparing the income sources

If you’re looking for yield from shares, then the location of those companies has an impact on how much end income you’ll receive. Of course, this should not be the only factor in determining your asset mix, but it is an important consideration when building a portfolio designed for income rather than capital growth.

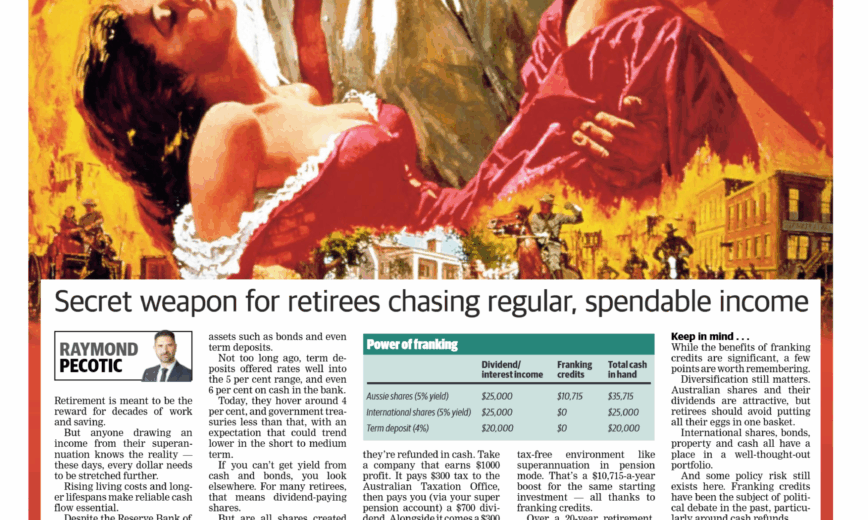

Here’s what $500,000 invested in different asset classes looks like at a 5% dividend yield (or 4% for term deposits) in a tax free environment like superannuation in pension mode.

| Dividend / Interest income | Franking credits | Total cash in hand | |

| Aussie shares (5% yield) | $25 000 | $10 715 | $35 715 |

| International shares (5% yield) | $25 000 | $0 | $25 000 |

| Term deposit (4%) | $20 000 | $0 | $20 000 |

That’s a $10 715 per annum boost for the same starting investment – all thanks to franking credits.

Over a 20-year retirement, that’s more than $200,000 in extra cash.

Why retirees skew local

While international equities may historically offer higher long term growth, and term deposits provide safety, only Australian shares can deliver cash refunds on dividends through franking credits. Few countries in the world have a system like ours. This system was designed to encourage Australians to invest in local companies, knowing they won’t be taxed twice on the same dollar of profit. That’s why income focussed retirement portfolios tend to hold a meaningful proportion of Aussie shares – they generate regular, spendable income that helps keep retirement budgets comfortable, even when interest rates remain low.

Things to keep in mind

While the benefits of franking credits are significant, a few points are worth remembering.

Diversification still matters. Australian shares and their dividends are attractive, but retirees should avoid putting all their eggs in one basket. International shares, bonds, property and cash all have a place in a well thought out portfolio.

And some policy risk still exists here. Franking credits have been the subject of political debate in the past, particularly around cash refunds. Proposals in recent elections to scrap them have been hotly debated and ultimately rejected by the electorate. So while the system remains intact today, retirees should be mindful that tax laws can change over time.

Like all things financial, there is no one size fits all approach when it comes to building retirement income portfolios. Professional advice is vital at this stage of life.

The interaction between franking credits, superannuation and personal tax situations can be complex, and speaking with a qualified financial adviser can assist retirees to utilise the benefits while avoiding any unintended consequences.

Currently, Perth is the capital city that our research is driving our clients to for optimal investment outcomes. Keep an eye out for our upcoming report on Victoria, and the opportunities we feel this market will present from early to mid-2025. CPA Property Reports are the ultimate research tool for those considering an investment into the any Australian property market.